Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

Disclaimer:

Registration granted by SEBI, enlistment with exchange and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

Krsnaa Diagnostics Ltd : Value Diagnosed 01-11-2023

The Indian diagnostic industry is expected to be supported by various fundamental growth drivers like the ageing population, rising awareness for healthcare, penetration in rural areas, as well as increasing investment by both government and private players. The industry is expected to grow at a CAGR of around 15% for the next few years, which presents a huge opportunity size.

With increasing government focus on providing high quality healthcare services, the rising prevalence of schemes like Ayushman Bharat, it is expected to boost the PPP (Public-Private Partnership) model in the diagnostic industry and Krsnaa’s business fundamentals are fully aligned to tap in this growing opportunity.

Krsnaa Business Model:

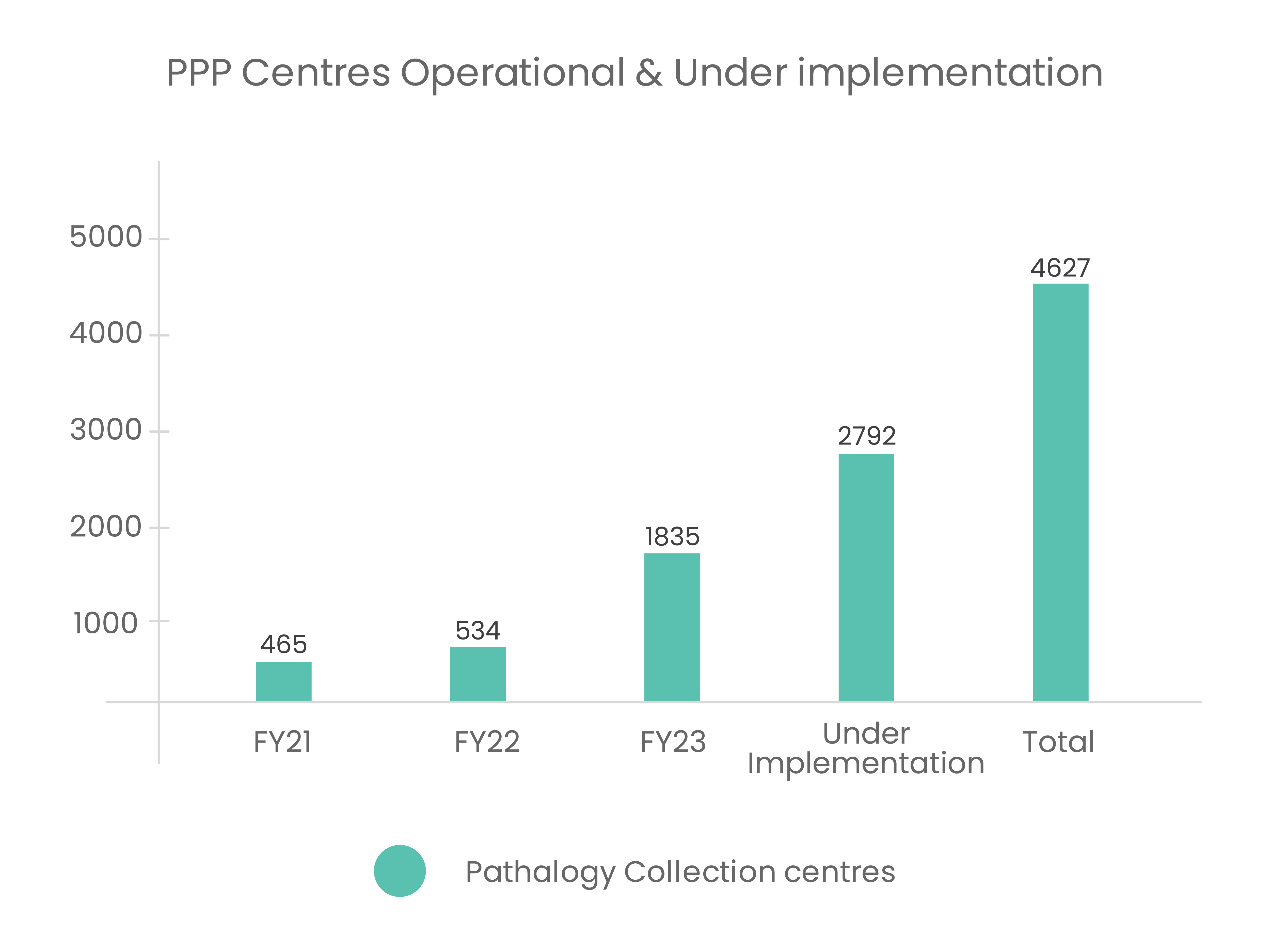

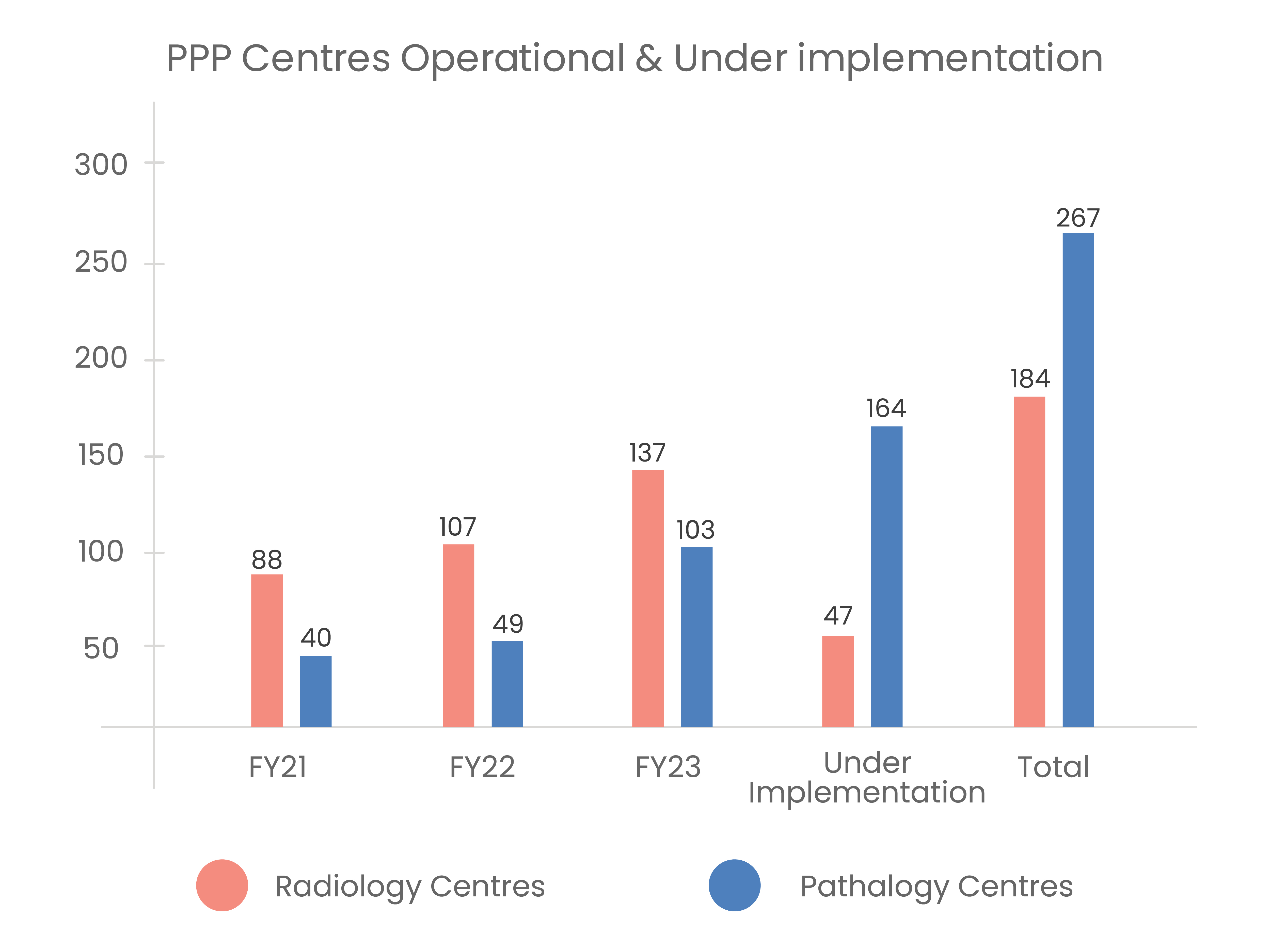

The company provides Radiology, Pathology and Tele-Radiology services. It has a leadership role as a PPP diagnostic entity, boasting 134 radiology centres, 1,370 tele-reporting centres, 105 pathology processing labs, and an extensive network of 1,336 pathology collection centres. The 3 important dimension of its business model are:

B2G (Business to Government):The diagnostic industry is highly underpenetrated in large part of our country. To address this gap, the government engages with private partners to collaborate with public hospitals and expand the reach of essential diagnostic services. Krsnaa, with its high quality services and disruptive prices, has emerged as a preferred partner for public health agencies. It has the largest presence in the diagnostics B2G segment. Thing about B2G is that you don’t have to open a big centre and then spend on marketing and then have a big gestation period to get decent volumes. Pathology centres in B2G are placed at captive hospitals premises which are already running at a lush of volumes, here Krsnaa comes in, bring in efficiency from its experience and capability of running large volumes. It de-stresses the stressed government infrastructure and ensures service quality is maintained. This segment contributes 70%+ to its overall revenues (Non-Covid).

B2B (Business to Business) : In addition to the PPP model, Krsnaa also have strategic tie-ups with various private hospitals. Generally, hospitals prefer to outsource their tests rather than set up an in-house laboratory testing facility. Tertiary hospitals, which may not have the equipment to conduct advanced tests, may also send samples to other high-end labs. Given that equipment for advanced tests is expensive, many hospitals find it economically unviable to operate them owing to low testing volume. In this model as well, Krsnaa enters into a contract with private healthcare companies, who provide space in their hospital, and Krsnaa sets up the Radiology and Pathology centres on a revenue sharing model which typically is about 20-30%. B2B segment forms 10%+ of its overall revenues.

B2C (Business to Consumer): Krsnaa with its focus on the B2G & B2B business has gained strong reach due to word of mouth publicity. With help of this, B2C is the new segment that Krsnaa is trying to build. It wants to leverage its existing network of labs and centres and spread them more through initiatives like Wellness packages wherein large number of tests are bundled together at prices that are higher than what it charges in the B2G & B2B segment, but it also includes services like home visit which is a good value proposition for well off customers like upper middle-class segment of the market who are not fine with visiting government hospitals and can afford to pay higher prices. This is a relatively high margin business but it involves having a franchise with revenue sharing arrangement and high gestation period. It still has high incremental benefits because it will help Krsnaa make better use of its existing level of capacities that it has built. Krsnaa recently launched its home collection services in Punjab, which is another initiative, which allows it to go to the doors of the citizens, and provide them with all collection services, which is over and above the patients who come to the government centre. The company is keen on expanding these to other states, including Maharashtra, Orissa, and Assam, where it already has pathology labs. B2C is recently launched and we estimate it contributes less than 10% to its revenues.

Value proposition:

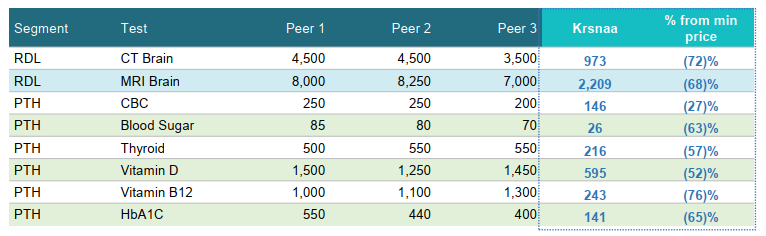

Krsnaa offers quality diagnostic services at disruptive prices. Its tests are almost 40% to 70% lower than the market rates which makes it a good value proposition for low-income households.

(Source: Company reports)

Despite these lower prices, the company has been able to deliver healthy operating margins which are equivalent to its peers.It has been able to do this because of the following reasons:

Zero doctor referrals fees for patient acquisition and limited expenses incurred in marketing and promotion which can be as high as 30% for its peers.

The company has tie-ups with Wipro GE Healthcare, Siemens Healthcare and Fujifilm India. Due to large procurement, equipment is purchased at lower cost and maintenance contracts are availed at discounts. Thus, setup costs are 10-15% lower than competitors.

Zero rentals to government hospitals for providing the space and availability of subsidized utility and electricity rates.

In the pathology segment, volumes play a significant role in pricing for reagents & kits for testing, due to its large volume requirements it is able to get a good bargain on its variable costs.

Competitive Advantage:

Volume Stability: Long-term of contracts (3-5 years for Pathology & 7-10 years for radiology) with inbuilt price escalation mechanism of 3-7% ensures higher and consistent visibility of revenues.

Diversified Revenue base: Krsnaa’s business comes from 14 states. Even though some states contribute higher to revenues at the moment, there are new states coming into picture and thus the business shall become more diverse going forward.

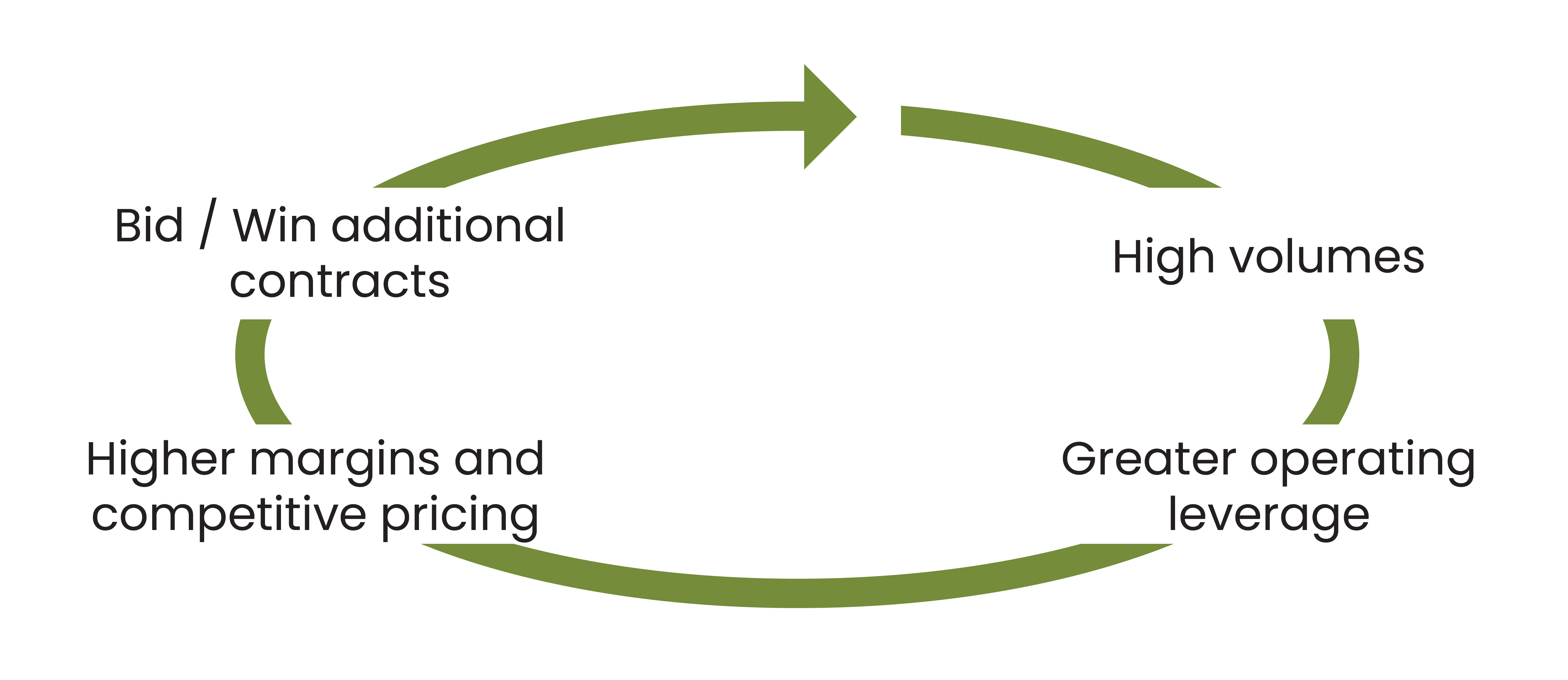

Tender winning capability: Existing investment in equipment and infrastructure, large scale of operations and cost competitiveness has resulted in strong bid-win rate of 79% with 100% technical qualification in the past.

The loop of low cost due to high volumes & additional contract wins due to being the lowest-cost provider works as follows:

(Source: Company reports)

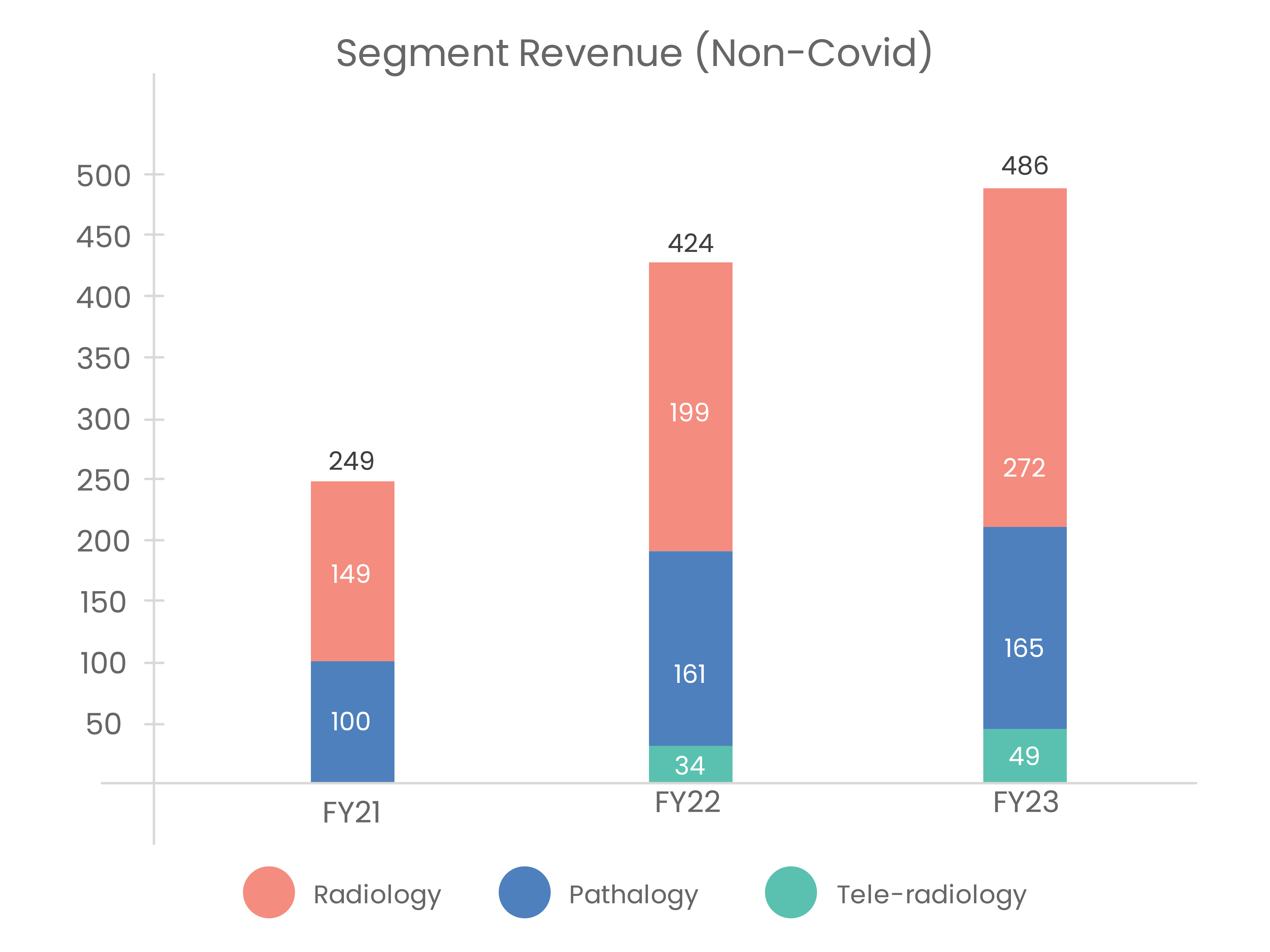

Segment-wise Business Performance:

(Source: Company Reports, Moneyworks4me research)

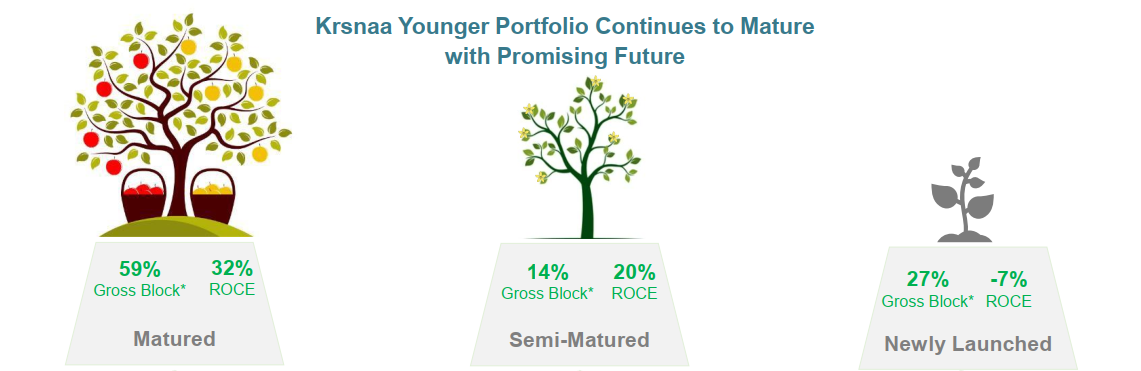

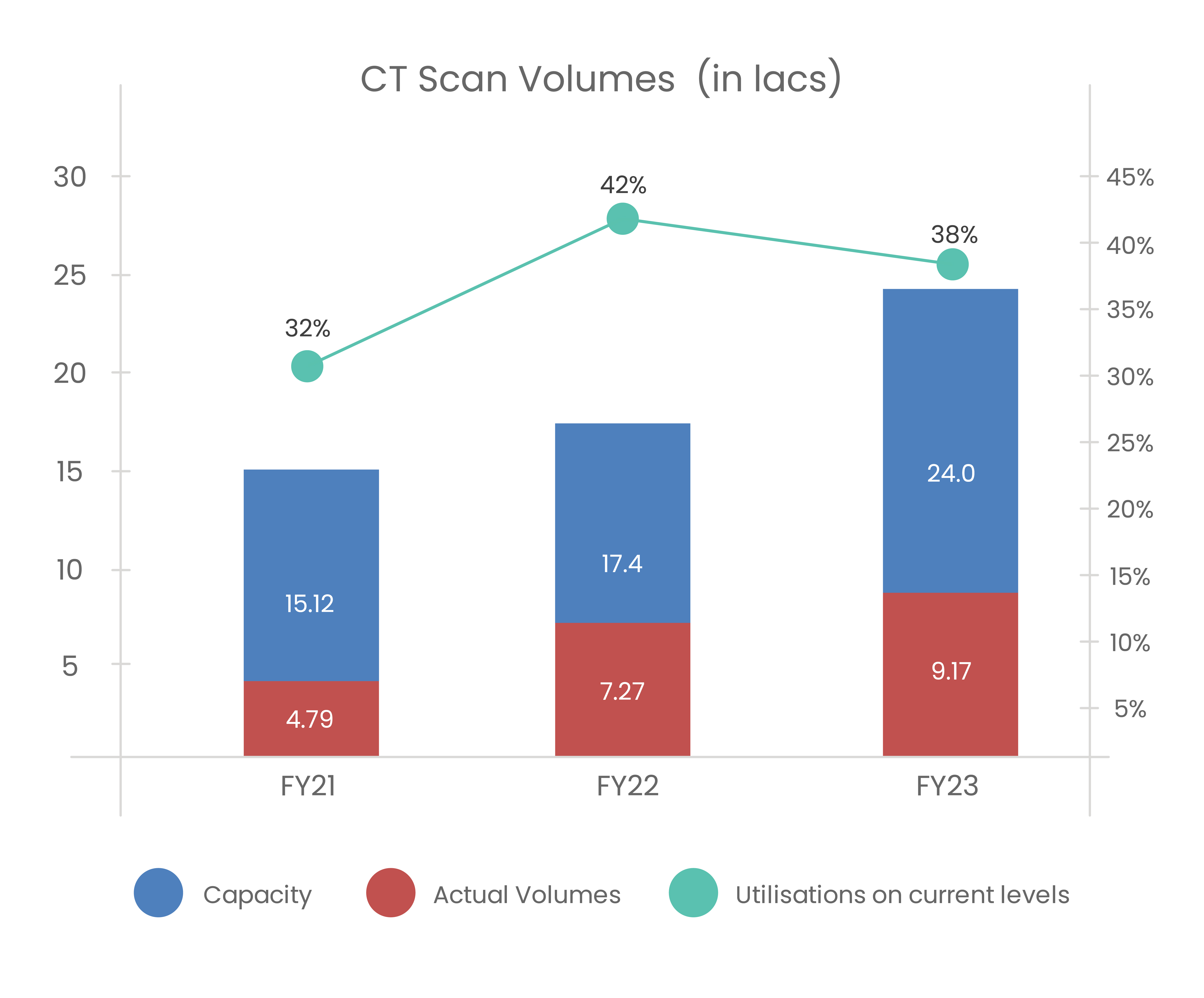

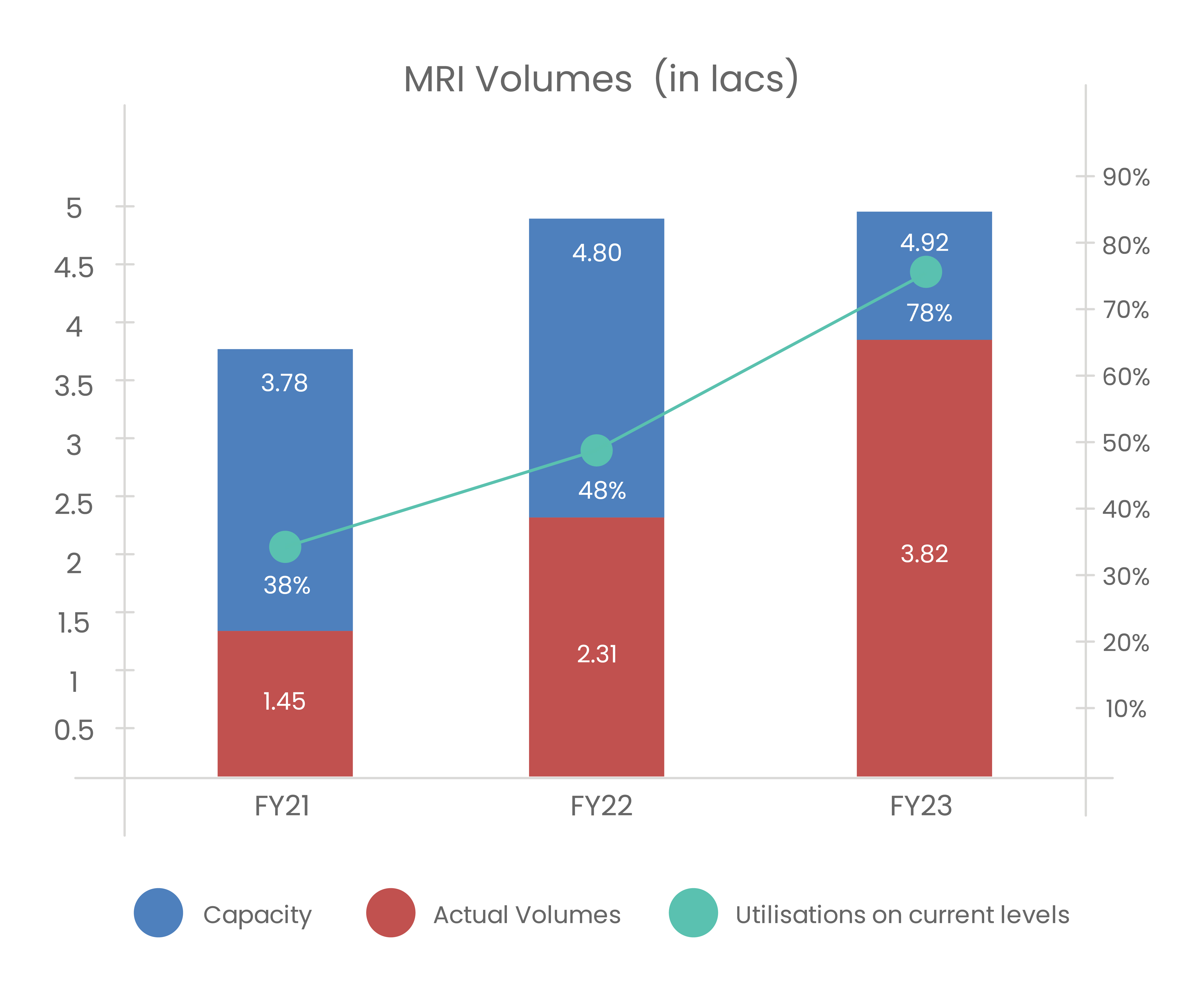

Radiology Segment: This includes CT Scans, MRI, Sonography, Mammography and X-rays. Machinery costs are high in this segment (~2 Cr for a CT scan machine & ~6 Cr for an MRI machine) while variable costs are very low. Once Radiology centres reach optimum utilisation levels (~60-70%) is when we get high ROCE from these centres. The maturity profile for the company’s radiology centers is outlined below.

(Source: Company reports)

Radiology segment has been growing at a CAGR of 36% from FY18 to FY23. Newly launched centres reaching semi-matured stage shall provide a high incremental ROCE for the company going forward.

(Source: Company Reports, Moneyworks4me research)

(Source: Company Reports, Moneyworks4me research)

Pathology Segment: This includes Routine Testing (Microbiology, Histopathology, Serology and Immunoassay) and Specialized Testing (Biochemistry, Molecular Biology, Oncology Genomics and personalized precision-based medicine). Capital outlay in this segment is significantly lower as against the Radiology segment. Major costs are Reagents and testing kits (20-25%).

(Source: Company Reports, Moneyworks4me research)

Pathology segment has been growing at a CAGR of 33% from FY18 to FY23. Recently secured tender are dominated by Pathology and thus this segment shall form a significant part of the company’s future revenues.

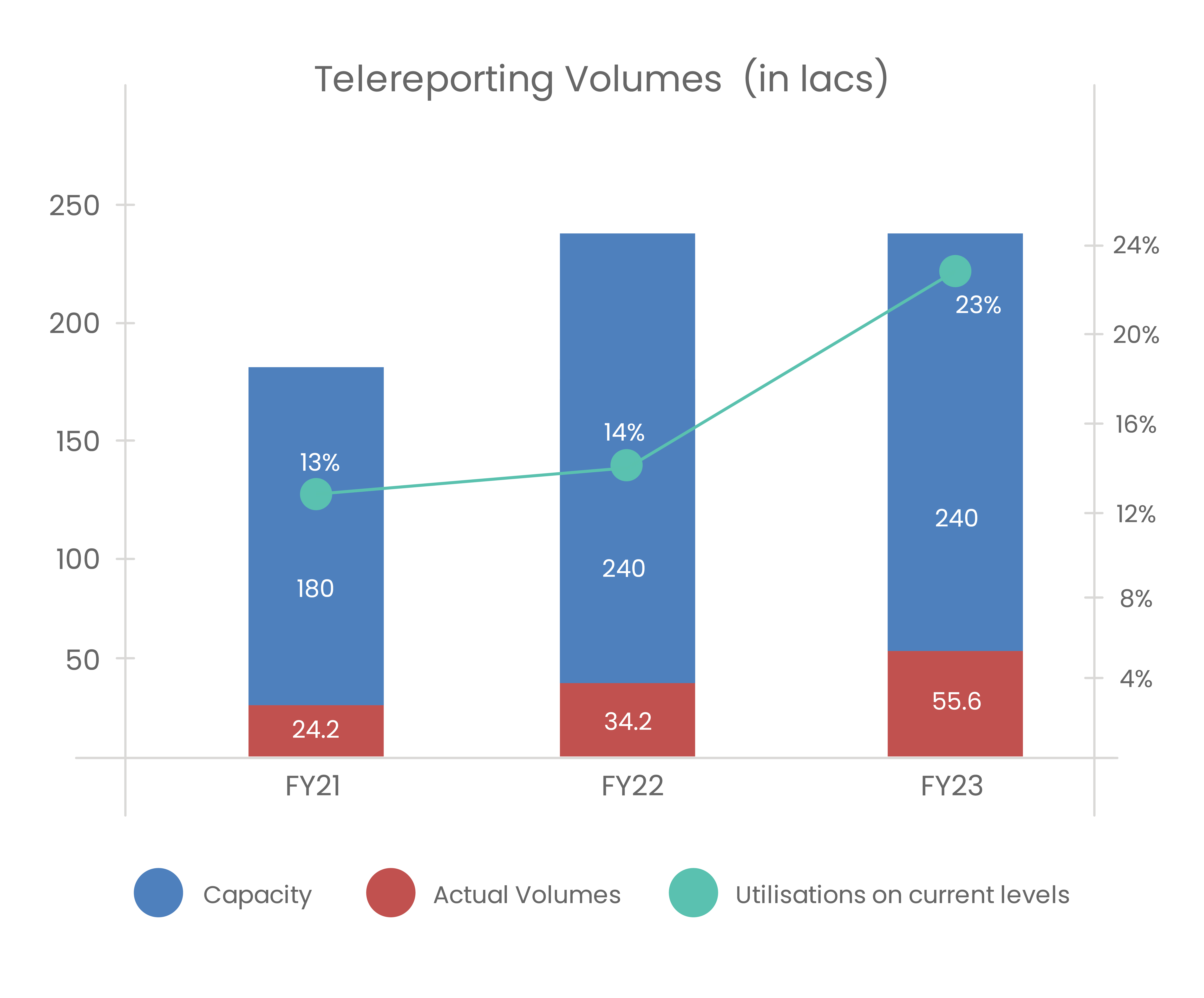

Tele-reporting Segment:

Krsnaa’s Tele-radiology services which it operates from Pune, is one of India's largest Tele-radiology reporting hub. At this facility, it has a team of 240+ radiologists from India and abroad, wherein it examines digital images and prepares reports. It provides 24x7 uninterrupted connectivity between diagnostic centers and the hub. This is a unique proposition that addresses the issue of shortage of full-time doctors and staff in the diagnostic industry. It also considerably increases the turnaround time for the reports. In addition, it also allows it to serve patients in remote locations where diagnostic facilities are limited.

(Source: Company Reports, Moneyworks4me research)

In FY23, the Tele-radiology segment had a revenue contribution of Rs. 49 Cr. However, Reporting costs associated with the tele-reporting segment were Rs. 52 Cr which implies that the segment is making nominal losses at the moment as there are significant fixed costs associated with maintaining such a setup. Currently, utilisation in the Tele-reporting segment is low as seen in the radiology capacity utilisation matrix provided below, but it is improving at a fast pace and soon the segment will provide a lift to the margin profile.

Concerns:

Delayed receivables from state authorities: In B2G business, payment from state governments getting delayed is the most common concern. The company's transparent data reporting and real-time data sharing with government authorities ensure periodic audits, providing confidence in their numbers. Additionally, their recoveries are supported by the National Health Mission, known for timely payments. Government tenders now include clauses allowing vendors to suspend operations if payments are delayed, indicating the government's commitment to addressing this issue. While procedural delays are common, there's no significant challenge foreseen in the future.

Re-tender risk: As tenders reach their expiration, if the counterparty is not interested in extending the contracts, we might see a sudden dip in revenue and cost escalation with respect to moving the owned machinery to a different center. As of now, there isn’t any big tender coming up for expiration.

Lower Utilisations at new centers: The company is undergoing a significant capex investment in the tender it has won, if the utilisations in the new location do not reach the optimum level, the company might go on diluting its ROE in search of revenue growth.

Levers for Growth:

Operationalizing tenders under implementation:

The company is set to deploy & commercialize significant resources in the states of Maharashtra, Rajasthan, Assam, & UP as provided below:

(Source: Company Reports, Moneyworks4me research)

The Rajasthan project hurdles have finally been removed, The Government of Rajasthan earlier had proposed to implement the project in 33 districts only, which it has now increased to 50 districts in total. The expected revenue from this project alone could be to the tune of Rs. 250-300 Cr per year (3 years contract with 2 years extension optional between the parties)

The company has recently secured a significant tender in the state of Assam. This project encompasses a network of 10 laboratories and 1,256 collection centers, significantly boostingits growth prospects in the northern-eastern region of the country, where government healthcare holds an 80% share.

(Source: Company Reports, Moneyworks4me research)

Capex outlay in FY 24 & 25 for the above project is Rs. 120-130 Cr per year. This shall keep ROE diluted in the meantime. The key thing to focus on here is that once all the capex is done and these facilities reach considerable utilisation, how big a size the company can become.

Scope of winning new tenders:

Due to its existing investment in equipment, large scale of operations and cost competitiveness, Krsnaa has a strong bid-win rate of 79% with 100% technical qualification in the past. Tender contracts typically range between 3-5 years for Pathology and go to about 10 years in the Radiology segments. The ability to quote attractive pricing at the time of renewal and a track record of successfully renewing the contract provides them revenue visibility in terms of tenure as well as gives a high chance of renewal.

Presently company is present in 14 states; however majority of the revenue (44%) comes from the West region. In some of the states where it already has a presence, the size of the contracts is very small. Their strategy involves both organic and inorganic growth. They plan to expand organically by partnering with public health agencies, private hospitals, medical colleges, and community health centers. Inorganically, they aim to make value-enhancing acquisitions to consolidate their business and leadership position. There are quite a few states currently that aren’t yet on the bandwagon of the PPP model in hospitals, their coming in will provide further scope for the growth of the company.

Disclosure: MoneyWorks4me's employees may have exposure in the securities mentioned in the above report. For detailed disclosure click here.

MoneyWorks4Me is a SEBI-registered Investment Adviser (IA) dedicated to helping investors build long-term wealth through transparent, research-driven, conflict-free guidance. Founded in 2008, we started our journey as a Research Analyst (RA), providing deep fundamental analysis, intrinsic value insights, and long-term investing frameworks for Indian equities. In 2017, we transitioned to a full-fledged SEBI-registered Investment Adviser, strengthening our commitment to acting as a fiduciary—always putting the investor’s interest first.

Our Vision

To become India’s most trusted, research-powered fiduciary advisory platform—where every investor, regardless of experience, can make calm, confident, and well-reasoned investment decisions.

What Makes MoneyWorks4Me Different

Fiduciary-first advisory model.

As SEBI-registered IAs, we are legally and ethically bound to act in the best interests of our clients. We do not sell or distribute any financial products. This ensures our guidance is 100% unbiased and conflict-free.

Deep fundamental research + robust valuation discipline.

Built on more than 15 years of equity research, our framework combines quality assessment, intrinsic value estimation, and a sensible margin-of-safety approach.

Process—not predictions.

We don’t rely on guesswork or market timing. Instead, we focus on asset allocation, risk management, and long-term compounding.

Technology + Human Intelligence.

We believe a combination of both is essential for investing success. We constantly innovate and upgrade in-house tools, financial X-rays, and portfolio analytics so that our team of analysts and advisors are equipped with the best.

Partner with Clients.

We follow a DIWM (Do-It-With-Me) approach where we partner clients in setting goals, financial planning, educating on our investing process and share decision-enabling resources transparently with our clients who retain control on execution.

Our Approach: Ensuring compounding work its magic on client portfolio.

MoneyWorks4Me ensures this through:

Investing in stocks, mutual funds, debt, and gold

Quality-at-Reasonable-Price way of investing in stocks

Constructing Direct Stock Portfolios with Core, Booster, and Amplifier stocks

A Mutual Fund Portfolio that delivers consistent out-performance and meaningful diversification (low overlap)

Periodic review and rebalancing

Clear Buy-Sell-Hold, and Position-sizing frameworks

MoneyWorks4Me method for rating and ranking mutual funds for SIP

MoneyWorks4Me rating and ranking of funds for SIP is available to subscribers only. Moneyworks4Me is not a rating and

ranking agency, however it is required that users have a way of selecting funds and building a Portfolio. The method used by it are described below to enable users to understand the logic behind the rating and ranking Subscriber will find more details on this in the

various content made available from time to time. In case you need more please write to besafe@moneyworks4Me.com

MoneyWorks4Me rates and ranks mutual funds based on the following data-driven system:

Performance Consistency: This is measure based on whether the fund has beaten the benchmark index consistently. For

this we compare the 3-year rolling returns of the fund with the benchmark for a minimum of 5 years and preferable 10

years. The period of rolling is one month and holding period is 3 years. Fund are color-coded Green on Performance when

the fund beats the benchmark more than 90% of the time. It is Orange if it beats 80% to 90% of the time and Red if less

than 80%. Funds with less than 5 year data are color-coded Grey.

Quality of Portfolio Holding: Moneyworks4Me has color-coded stocks as Green, Orange and Red based on whether the

company's performance has generated a ROCE above a threshold level (cost of capital) over 10 years (minimum 6 years) and

generated positive Free Cash Flow. For Banks it checks whether ROE is greater than 15% and sales has grown over previous

year. Stocks that perform consistently on these combined metrics are color-coded Green (min score 14 out of 20), Orange

(between 8 and 14) and Red (less than 8 out of 20).

Fund are color-coded Green provided the portfolio has 70% holding in Green stocks but not more than 20% in Red stocks.

Funds with more than 20% Red stocks in the portfolio are color-coded Red. The rest are Orange funds

Funds ranking in screeners: Performance Consistency and Quality are two parameters used for ranking funds for SIP. The

ranking as follows GG, GO, GR, OG, OO, OR, RG, RO and RR.

With the same color-coded funds, the one with the higher Average 3-year rolling returns (over 5 to 10 years), the number

that appears in the Performance tag, ranks higher.

Here is the summary:

The third tag Upside Potential is not relevant for SIP. It is relevant for lumpsum investments in Mutual Funds.

Make an informed decision for Stocks

Invest using an intelligent system with powerful data-driven tools that help you identify opportunities and make informed buy-hold-sell decisions

You can make an informed decision based on:

Q : Quality :- Q Very Good

Q Somewhat Good

Q Not Good

V : Valuation:- V+UnderValued (UV) V Somewhat UV

V Fair Value

V Somewhat OV

V+ OverValued (OV)

Buy quality Stocks when they are available at reasonable prices and supported by an upward price trend and Sell when they are Overvalued using the Decizen Rating System. Covers 3500+ stocks

Make an informed decision for Funds

You can make an informed decision based on:

P : Performance (%)* 14 Very Good

14 Somewhat Good

12 Not Good

Less than 5 year data

Q : Quality of Holding Q Very Good

Q Somewhat Good

Q Not Good